What is Claims Management? Complete Guide 2025

Have you ever experienced an insurance claim that took a very long time to be processed or was more complicated than you thought? If yes, you’re definitely not the only one. Actually, one of the most common reasons for people’s dissatisfaction with insurance is the delay of their claims and the confusion that arises from them.

But do you realize that claims management is the one main process that is actually working behind the scenes, without being noticed, and enabling the rest of the experience to go smoothly?

Claims management is the mechanism that keeps the insurance industry going. It is the one that makes sure that any claim, be it for health, auto, or property, is dealt with in a timely, accurate, and fair manner to the claimant. If this system were absent, the whole insurance system would hardly be able to work efficiently

In this blog, we’ll break down what claims management really means and why it is important.

What is an Insurance Claim?

An insurance claim is basically a formal request made by you to an insurance company after you have suffered a loss or damage for which you have insurance. The claim is the way to ask the insurer to reimburse the costs of what has been agreed, be it hospital expenses, car repairs, or damage to your property.

In case you are involved in a car accident, you would ask your car insurance provider to cover your repair costs by filing a claim with them. Similarly, if you have a surgery that is covered by your health insurance, then your hospital (or you) would file a claim to get the money back that has been spent on the surgery.

In simple terms, an insurance claim is the way by which you “turn on” your policy benefits. It’s the very moment when your monthly premiums become a real and tangible financial assistance to you when you are in dire need.

What is Claims Management in Insurance?

Claims management is the complete process of handling, reviewing, and settling insurance claims from the moment they are reported until they are closed. It’s how insurance companies make sure claims are valid, accurate, and paid out fairly to the right person.

Basically, it is the link connecting the policyholder and the insurer. Through it, the company whose customer has lodged a claim can be assured that everything from document validation to damage evaluation and payment issuance is carried out in a timely and organized way.

For insurance companies, efficient claims management helps build trust and transparency with clients. For policyholders, it means faster settlements, fewer errors, and less stress during already challenging times.

How Does the Claims Management Process Work?

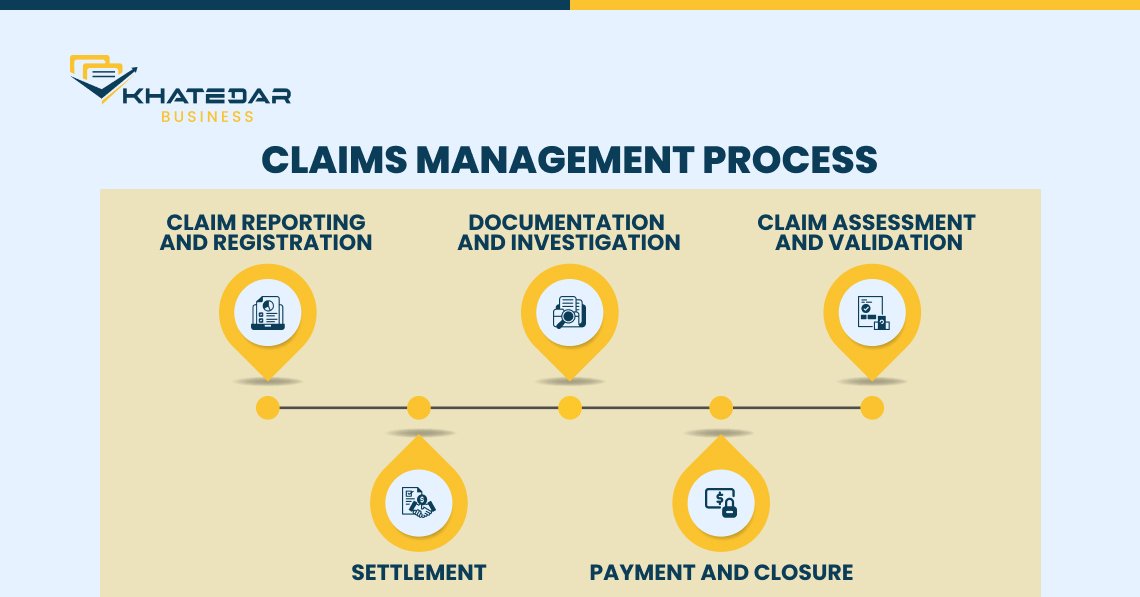

The claims management process sounds complex, but when broken down, it follows a clear step-by-step flow.

1. Claim Reporting and Registration

It all starts when a policyholder reports a claim to their insurance company. This could be through a call, email, app, or online portal. The insurer notes the scene, time, and the extent of the loss or damage. After obtaining the information, a claim is officially recorded, and a unique claim number is created for tracking purposes.

2. Documentation and Investigation

Insurance firms, after recording a claim, require different documents that may include the bills, receipts, medical reports, or police statements, depending on the nature of the claim. To get the truth of the claim, the investigation stage follows. Insurers send surveyors or adjusters to inspect the damage or confirm facts.

3. Claim Assessment and Validation

The insurance company then carefully reviews the details submitted by the policyholder. They estimate the loss and confirm if it is in line with the terms of the insurance policy. At this point, it is verified that the claim is valid and accurate and not fraudulent. The confirmation stage is followed by the approval stage if all is well.

4. Settlement

The moment a claim is valid, the insurance company calculates the amount of money it will give as compensation. Repairing, replacing, or paying for medical bills can all be a part of the settlement. The main point is to guarantee the policyholder receives the money they’re entitled to.

5. Payment and Closure

In the end, the insurer completes the payment formalities and notifies the claimant about it. The claim is considered “closed” when the payment is both made and acknowledged. However, insurers keep a record for future reference or audits.

Final Thoughts

Claim management sounds dull, but it is literally the core of the insurance world. This is the mechanism by which a written promise is transformed into tangible financial help in times of need. Every step from reporting a loss to getting compensation is a process that counts, and if it is done properly, it creates trust and loyalty to the insurers from their clients.

Good claims management is not only a matter of procedural correctness and optimization, it is also about equity, speed, and empathy. With this, insurers are able to keep their good name, while policyholders get the comfort that they are really protected.

We hope this blog gave you a clear understanding of what claims management is and why it’s so vital in the insurance industry.

Stay tuned for Part 2, where we’ll explore how outsourcing insurance claims can make the entire process faster, more efficient, and cost-effective.

FAQs

Q- What do you mean by claims management?

A- Claims management refers to the complete process of handling insurance claims, from reporting and verifying them to settlement and closure. It ensures claims are processed quickly, fairly, and according to policy terms.

Q- What does a claims management system do?

A- A claims management system helps insurers track, process, and manage claims efficiently using automation and data management tools. It reduces errors, speeds up settlements, and improves overall customer experience.

Q- What are the principles of claims management?

A- The main principles include fairness, transparency, accuracy, and efficiency. These ensure every claim is handled consistently, verified properly, and settled promptly while maintaining trust between insurer and policyholder.

Q- What are three types of claims?

A- The three common types of insurance claims are health claims, property claims, and auto claims. Each type deals with different kinds of losses but follows a similar process of verification, assessment, and settlement.